You need to consider paying off your house before you invest a dime. Why?

Because to invest before your house is paid for (outside of a 401k or retirement plan) is basically borrowing from your house to buy securities, stocks, bonds and mutual funds.

You are borrowing at 5% to hopefully get a return higher than 5% and pocket the difference. The key word is hopefully. A lot of things have to line up for that to work.

Guess who is propagating this theory?

Thats right, the brokerage industry. They want nothing to do with you paying off a mortgage. They need assets so they can collect commissions and fees!

I know its not very sexy to pay off your house and its cool to talk about your stockbroker or investment portfolio at parties but if you think logically for second, when you pay off your house, you are guaranteeing yourself 5% (or whatever your current mortgage rate is) and you just may enjoy a slightly less stressful life knowing your house is paid for.

Additionally, some states offer bankruptcy and lawsuit protection for your primary residence so thats nice, just in case.

Yes, I know you'd be missing out on the mortgage deduction come tax time but it has always seemed rather pitiful anyway but I am no tax guy.

December 16, 2010

December 7, 2010

What is #1 for Stockbrokers?

I came across a great article today which is exactly what I have been saying for years. Below is the headline.

What's No. 1 for Brokers?

Right now, securities firms don't have to put investors' interests first. New regulations may change that—and Wall Street isn't happy..

For those of you who have read my blog or book, this comes as no surprise but for those that haven't, I hope the title is a little shocking. You can read the entire article here.

Bottom line is that stockbrokers do not have to put their clients interests first, yes, you read that correctly and is why I have been pounding the table encouraging investors to learn how to invest for themselves.

Its actually quite easy and you'll know that the person who is handling your money is the person who cares about it the most, YOU!

What's No. 1 for Brokers?

Right now, securities firms don't have to put investors' interests first. New regulations may change that—and Wall Street isn't happy..

For those of you who have read my blog or book, this comes as no surprise but for those that haven't, I hope the title is a little shocking. You can read the entire article here.

Bottom line is that stockbrokers do not have to put their clients interests first, yes, you read that correctly and is why I have been pounding the table encouraging investors to learn how to invest for themselves.

Its actually quite easy and you'll know that the person who is handling your money is the person who cares about it the most, YOU!

November 30, 2010

Crazy Predictions

I'm pretty sure they make these outrageous predictions to get some press, which they sure seem to. No wonder I haven't sold as many books as I'd like :)

No crazy predictions here, just good solid rational thinking. Advice without an agenda.

It's really hard not to get caught up listening to all the noise so as Nike doesn't say, just don't do it :)

Remember, I am available for coaching, see here for more information or just keep up with this blog or buy my book.

November 19, 2010

Derivatives

99.9% of investors have no business with derivatives. If a financial guy suggests one to you, hang up the phone.

A derivative is a financial instrument whose value is some percentage of the future value of the underlying asset which is usually a stock, commodity or currency.

There are few instances when a derivative is appropriate for non-speculators. A good example is a cotton farmer hedging or locking in the current price of his crop. This lowers his risk.

Derivatives have become increasingly complex and more and more stockbrokers, financial advisors and planners are recommending them to their clients. Ouch! All you are doing is taking on more risk.

As with most financial products, they sound great but they are not and you have no business 'investing' in them.

A derivative is a financial instrument whose value is some percentage of the future value of the underlying asset which is usually a stock, commodity or currency.

There are few instances when a derivative is appropriate for non-speculators. A good example is a cotton farmer hedging or locking in the current price of his crop. This lowers his risk.

Derivatives have become increasingly complex and more and more stockbrokers, financial advisors and planners are recommending them to their clients. Ouch! All you are doing is taking on more risk.

As with most financial products, they sound great but they are not and you have no business 'investing' in them.

November 12, 2010

GM IPO (and all IPO's)

I was a stockbroker for a long time and in my experience, I learned simply that the best IPO's are held tightly by the Wall Street firms that do the underwriting. The worst IPO's are distributed to anyone and everyone. Interestingly, I could sell preferred stock via IPO all day and hide the commission, more on that in another blog post.

There is an old saying on Wall Street, ''if you can get your hands on an IPO, you don't want it''.

IPO's are usually priced low enough so that the initial owner takes on very little risk. The irony is that successful IPO's are flipped (sold) by their original and very temporary owner (hedge funds, mutual funds, etc) to average investors who are likely to hold and own the shares over a longer period of time which is ultimately what the underwriters (investment banks) like to see.

So why don't the underwriters (investment banks) sell to average investors? Its simply payback time, for all the commissions that the hedge funds and mutual funds have generated.

October 25, 2010

Presidential Stock Market Cycle

History shows us that there is some correlation between the election cycle and stock market (S&P 500) results.

Typically, the 3rd year of the Presidents term, regardless of party, is the strongest, followed by the 4th, the 1st and the 2nd. There is a great deal of theory as to why this is so but nothing concrete. It should be noted that there are huge variances in these results as well.

Since 1942, the 200 days following the midterm elections have produced an average of 18% gain.

What does this mean to you? NOTHING.

If I told you that the first day of the month produces more than average returns (which it seems to), would you go out buy stocks because of that? I hope not.

Bottom line is that as tempting as it is to time the market, its just simply foolish to try.

Stick to buying a very low cost index fund or ETF and adding to it as often as you can and with that simple strategy, you will beat over 95% of investors and over 90% of professional money managers who try. Why? Because fees are everything, not timing the market and not which stocks you buy.

Typically, the 3rd year of the Presidents term, regardless of party, is the strongest, followed by the 4th, the 1st and the 2nd. There is a great deal of theory as to why this is so but nothing concrete. It should be noted that there are huge variances in these results as well.

Since 1942, the 200 days following the midterm elections have produced an average of 18% gain.

What does this mean to you? NOTHING.

If I told you that the first day of the month produces more than average returns (which it seems to), would you go out buy stocks because of that? I hope not.

Bottom line is that as tempting as it is to time the market, its just simply foolish to try.

Stick to buying a very low cost index fund or ETF and adding to it as often as you can and with that simple strategy, you will beat over 95% of investors and over 90% of professional money managers who try. Why? Because fees are everything, not timing the market and not which stocks you buy.

October 12, 2010

Leverage

Leverage for the most part is bad, very bad. Leverage is simply multiplying the effects of what you are buying and it will cost you.

The most common leverage is the use of margin which is basically borrowing money from the brokerage firm who holds your stocks or mutual funds to buy more of the same. If stocks go up, you multiply the effects and can do very well however, the reverse is also true, and when stocks go down, you will not only have mutiplied that outcome but made it worse because you are paying to borrow money at the going rate, ouch.

Another common use of leverage is real estate and up until recently you needed 10-20% of the cost of the property and then borrowed the rest from the bank paying your mortgage and hoping the price of your house went up. This worked out well for years until the real estate bust of 2008. Before then, house prices slowly but surely always increased. We now know the painful truth that home price increases are not a guarantee and leverage in real estate can cause a terrible outcome.

Leverage can sometimes be great and we all know someone who bought land or real estate or margined stocks and did very well but quite frankly, those are rare instances. My advice is that leverage is not for everyone and if you can avoid it, do so. Pay off your house as soon as you can and do not borrow money against your stocks or mutual funds.

The most common leverage is the use of margin which is basically borrowing money from the brokerage firm who holds your stocks or mutual funds to buy more of the same. If stocks go up, you multiply the effects and can do very well however, the reverse is also true, and when stocks go down, you will not only have mutiplied that outcome but made it worse because you are paying to borrow money at the going rate, ouch.

Another common use of leverage is real estate and up until recently you needed 10-20% of the cost of the property and then borrowed the rest from the bank paying your mortgage and hoping the price of your house went up. This worked out well for years until the real estate bust of 2008. Before then, house prices slowly but surely always increased. We now know the painful truth that home price increases are not a guarantee and leverage in real estate can cause a terrible outcome.

Leverage can sometimes be great and we all know someone who bought land or real estate or margined stocks and did very well but quite frankly, those are rare instances. My advice is that leverage is not for everyone and if you can avoid it, do so. Pay off your house as soon as you can and do not borrow money against your stocks or mutual funds.

October 6, 2010

Mutual Fund Price Wars

To keep up with competitors, Vanguard announced that its Total Stock Market Index Fund, symbol VTSAX has lowered its minimum from 100k to 10k. This is wonderful news for investors. Its no secret that I love low fees and because of that, I love the Vanguard series of funds and etf's.

VTI is the Total Stock Market ETF whose fees are .07%. Now, most investors can buy into the mutual fund version of the same, VTSAX whose fees are likewise .07%.

Check out what low fees mean to you in the long term. You can access this from the yahoo finance profile of VTSAX here. Scroll down and look for fees and expenses. Below is what you will see. A comparison between VTSAX and the average fund in the category.

Fees & Expenses

Expense VTSAX Category Avg

Total Expense Ratio: 0.07% 1.11%

Max 12b1 Fee: N/A N/A

Max Front End Sales Load: N/A 5.27%

Max Deferred Sales Load: N/A 2.50%

3 Yr Expense Projection*: $23 $700

5 Yr Expense Projection*: $40 $1,114

10 Yr Expense Projection*: $90 $2,224

* Per $10,000 invested

So the question to you is, would you rather pay $90 or $2,224 (for every 10k invested) ?????

And to add insult to injury, most stockbrokers and financial advisors will charge you another 1%-2% on top of that.

VTI is the Total Stock Market ETF whose fees are .07%. Now, most investors can buy into the mutual fund version of the same, VTSAX whose fees are likewise .07%.

Check out what low fees mean to you in the long term. You can access this from the yahoo finance profile of VTSAX here. Scroll down and look for fees and expenses. Below is what you will see. A comparison between VTSAX and the average fund in the category.

Fees & Expenses

Expense VTSAX Category Avg

Total Expense Ratio: 0.07% 1.11%

Max 12b1 Fee: N/A N/A

Max Front End Sales Load: N/A 5.27%

Max Deferred Sales Load: N/A 2.50%

3 Yr Expense Projection*: $23 $700

5 Yr Expense Projection*: $40 $1,114

10 Yr Expense Projection*: $90 $2,224

* Per $10,000 invested

So the question to you is, would you rather pay $90 or $2,224 (for every 10k invested) ?????

And to add insult to injury, most stockbrokers and financial advisors will charge you another 1%-2% on top of that.

September 23, 2010

Jim Cramer Results Vs S&P 500

Its very tempting to want to trade stocks. Its very natural to want to be an active investor. The irony is that the passive investor beats the active investor all the time over a reasonably timeframe.

Jim Cramer (Mad Money) is very informative and certainly fun to watch however I read recently that he has beaten the S&P 500 just a few years as a commentator and when you consider the amount of commissions, even at $7 per trade, you really don't end up making more following his trades versus the S&P 500. Additionally, the capital you would need to follow his recommendations is too large for most investors so you have to pick and choose and you know how that goes, you will invariably pick the losers :(

To be fair, Jim Cramer has claimed that his hedge fund beat the S&P 500 over its twelve year run, although, this has never been verified and its important to point out that he wasn't the only stock picker.

Its boring but buying the S&P 500 when you feel like it and adding to it over time is THE winning strategy, period. Sure, you can lose money that way too but at least you can sleep at night knowing that with that strategy, you will beat over 90% of the professional money managers over the long haul.

Jim Cramer (Mad Money) is very informative and certainly fun to watch however I read recently that he has beaten the S&P 500 just a few years as a commentator and when you consider the amount of commissions, even at $7 per trade, you really don't end up making more following his trades versus the S&P 500. Additionally, the capital you would need to follow his recommendations is too large for most investors so you have to pick and choose and you know how that goes, you will invariably pick the losers :(

To be fair, Jim Cramer has claimed that his hedge fund beat the S&P 500 over its twelve year run, although, this has never been verified and its important to point out that he wasn't the only stock picker.

Its boring but buying the S&P 500 when you feel like it and adding to it over time is THE winning strategy, period. Sure, you can lose money that way too but at least you can sleep at night knowing that with that strategy, you will beat over 90% of the professional money managers over the long haul.

September 3, 2010

Cash and your Stockbroker

Do you know why your stockbroker hates cash?

Because he doesn't get paid when you have cash on the books.

Its stating the obvious but stockbrokers and financial advisors get paid to invest your money, period. Not watch it. That's right, stockbrokers get paid only when you are invested, period. They get paid either by commission when they buy something for your account or as a percentage of invested assets. Neither of which is cash in your account.

This is a huge conflict on interest, in my opinion. Think about it. You send him some cash after a nice bonus and the market maybe looks tenious at the moment. What do you think happens next? Thats right, you get the call. We need to invest this right away, and if that happens near the end of the commission month, well, you know the rest of the story.

This is just another reason that you need to handle your own finances. Its not hard. Its easy. And you can rest assured that your account is in the hands of the person who cares about it the most, you.

Because he doesn't get paid when you have cash on the books.

Its stating the obvious but stockbrokers and financial advisors get paid to invest your money, period. Not watch it. That's right, stockbrokers get paid only when you are invested, period. They get paid either by commission when they buy something for your account or as a percentage of invested assets. Neither of which is cash in your account.

This is a huge conflict on interest, in my opinion. Think about it. You send him some cash after a nice bonus and the market maybe looks tenious at the moment. What do you think happens next? Thats right, you get the call. We need to invest this right away, and if that happens near the end of the commission month, well, you know the rest of the story.

This is just another reason that you need to handle your own finances. Its not hard. Its easy. And you can rest assured that your account is in the hands of the person who cares about it the most, you.

August 18, 2010

Patience (Investing)

It never was my thinking that made the big money for me. It was always my sitting. Got that? My sitting tight! -Edwin Lefevre

This blunt warning was issued in Lefevre's 1923 fictional memoir, and treated by many financial advisers like the Bible. Some 77 years later, behavioral finance professors Terrance Odean and Brad Barber's research into transactions by some 66,000 households between 1991 and 1996 found that those who traded least earned seven percentage points a year more than the most frequent traders. Fast forward 10 more years and here we are, nothing has changed except that costs to own the market via an index are even more cost effective!

The moral: Once you arrange your assets into your ideal allocation, don't tinker. Rebalance once a year to keep your mix on track, but otherwise, sit tight.

This blunt warning was issued in Lefevre's 1923 fictional memoir, and treated by many financial advisers like the Bible. Some 77 years later, behavioral finance professors Terrance Odean and Brad Barber's research into transactions by some 66,000 households between 1991 and 1996 found that those who traded least earned seven percentage points a year more than the most frequent traders. Fast forward 10 more years and here we are, nothing has changed except that costs to own the market via an index are even more cost effective!

The moral: Once you arrange your assets into your ideal allocation, don't tinker. Rebalance once a year to keep your mix on track, but otherwise, sit tight.

August 16, 2010

A Lot Of Retirement Is Luck

As a former stockbroker / financial planner, I hate to admit it but a lot of retirement is luck. Saving for retirement is extremely important BUT planning is not.

You can easily see what I mean. Imagine two people with basically the same incomes (adjusted for inflation) and one person retires in 1980 and parks the bulk of their retirement money in safe CD's paying 15%! Now that is good timing but is really just plain luck, not planning.

Imagine a second guy who retired just a few years ago, in 2008, ouch, first off, he likely lost some of his retirement money in his 401k or IRA and then had the unfortunate timing to choose between a stock market that is pretty darn scary or a CD or other fixed income paying virtually nothing. This is also luck, bad luck, but again, has nothing to do with planning.

The point is that while planning is fine idea and looks good on paper, its really a useless exercise with little value. Financial planning is propagated by the investerati to keep your assets under their control.

A better idea is to be fiscally prudent (buy what you can afford), save what you can when you can (set a goal of 10%-15%), don't stress too much about retirement and when it comes time to retire, then and only then can you truly plan.

Planning when retired (or within a year at most) is infinitely more accurate, you will know what assets you have, what liabilities you have and can adjust your lifestyle to match, its that simple. In my book, How the Investment Business Really Works, I offer a worksheet in the back of the book that will walk you through the simple steps to what I call Realistic Retirement.

You can easily see what I mean. Imagine two people with basically the same incomes (adjusted for inflation) and one person retires in 1980 and parks the bulk of their retirement money in safe CD's paying 15%! Now that is good timing but is really just plain luck, not planning.

Imagine a second guy who retired just a few years ago, in 2008, ouch, first off, he likely lost some of his retirement money in his 401k or IRA and then had the unfortunate timing to choose between a stock market that is pretty darn scary or a CD or other fixed income paying virtually nothing. This is also luck, bad luck, but again, has nothing to do with planning.

The point is that while planning is fine idea and looks good on paper, its really a useless exercise with little value. Financial planning is propagated by the investerati to keep your assets under their control.

A better idea is to be fiscally prudent (buy what you can afford), save what you can when you can (set a goal of 10%-15%), don't stress too much about retirement and when it comes time to retire, then and only then can you truly plan.

Planning when retired (or within a year at most) is infinitely more accurate, you will know what assets you have, what liabilities you have and can adjust your lifestyle to match, its that simple. In my book, How the Investment Business Really Works, I offer a worksheet in the back of the book that will walk you through the simple steps to what I call Realistic Retirement.

August 6, 2010

Google or Wikipedia Index Funds

If you were to google (search) for index funds, you will find a great number of answers. You will find some great companies offering what wasn't available just 40 years ago, an index fund.

If you search wikipedia for index fund, you will get a great explanation and a wonderful history lesson. It was only 1975 when John Bogle 'invented' and marketed the index fund to the public. Most thought he was crazy, why would investors be happy with 'average' returns. As it turns out, Bogle was crazy like a fox and now, some 35 years, investors are finally wising up to the fact that index funds routinely beat most mutual funds and certainly all stockbrokers and financial advisors.

The reason for the popularity of index funds is simple; ease of use and better performance. Add to that there is no conflict of interest as there can be utilizing a stockbroker or that you dont get caught up wasting time trying to chase the next best mutual fund, its easy to see.

If you search wikipedia for index fund, you will get a great explanation and a wonderful history lesson. It was only 1975 when John Bogle 'invented' and marketed the index fund to the public. Most thought he was crazy, why would investors be happy with 'average' returns. As it turns out, Bogle was crazy like a fox and now, some 35 years, investors are finally wising up to the fact that index funds routinely beat most mutual funds and certainly all stockbrokers and financial advisors.

The reason for the popularity of index funds is simple; ease of use and better performance. Add to that there is no conflict of interest as there can be utilizing a stockbroker or that you dont get caught up wasting time trying to chase the next best mutual fund, its easy to see.

July 30, 2010

Retirement Killers

Retirement is the number one goal of investors. Yet, looking at the numbers, it's clear that many investors are undermining their good intentions with unfortunate actions. Here are five mistakes to avoid if you want your retirement dreams to become a reality.

1. Cracking your nest egg before retirement. A study by Hewitt Associates found that 45% of workers cash in their 401(k)s when they switch jobs. In other words, they take the money -- paying income taxes and a 10% penalty if they're not yet 59 1/2 years old -- rather than leave it in a retirement account. That's no way to build the retirement of your dreams. When you change jobs, you can transfer the money in your employer-sponsored retirement plan to an IRA.

2. Spending your retirement savings too fast. If you've made it to retirement, congratulations. You've amassed enough money to create your own portfolio-generated paycheck. Excellent work. But you can't take it too easy, because you'll receive a severe pay cut if you deplete your portfolio too fast. How much can you take out each year and be almost certain that you won't outlive your savings? Just 4% a year. That's the withdrawal rate that would have sustained a mix of stocks and bonds over most 30-year historical periods. Sure, if you retire on the eve of the next bull market, you can take out more. However, if you quit working right before the next bear market, then taking out more than 4% a year could have your portfolio beating you to the grave.

3. Trying too hard to beat the market. You basically have two choices: You can be a master stock-picker like Warren Buffett or Peter Lynch and try to find the next Wal-Mart. Or you can broadly diversify your assets, mostly via low-cost index funds. This way, you enjoy hefty exposure to all the great companies.

4. Paying too much for help. There's nothing wrong with getting financial advice. But I firmly, strongly, passionately believe that such help should be objective and affordable. Paying too much for advice (especially if it's bad or at least conflicted) does a lot for your broker's retirement, not yours. Paying just 1% a year on a $100,000 portfolio over 20 years could result in your forking over more than that amount in fees. That's a hundred grand that could have been in your pocket. Of course, if the advice you received had your portfolio performing better than what you could do on your own, then the price might be worth it. But if you're paying 1% or 2% a year to lose to an index fund -- as most mutual fund managers do -- then you're better off taking control of your own investments.

5. Retiring permanently when you really just needed a break. If you're in your 60s, you should plan on living at least another two decades. Can you stand full-time leisure for 20 years? Sure, it may sound good now, but many retirees find they get pretty bored after a while. But by then, they have already severed many of their professional ties. Before you decide to retire fully and permanently, discuss a phased or gradual retirement with your employer and/or business partners. Or the possibility of working on a project basis, allowing you to take several months off each year. Or maybe just a one-year sabbatical. Explore your options before you no longer have them.

1. Cracking your nest egg before retirement. A study by Hewitt Associates found that 45% of workers cash in their 401(k)s when they switch jobs. In other words, they take the money -- paying income taxes and a 10% penalty if they're not yet 59 1/2 years old -- rather than leave it in a retirement account. That's no way to build the retirement of your dreams. When you change jobs, you can transfer the money in your employer-sponsored retirement plan to an IRA.

2. Spending your retirement savings too fast. If you've made it to retirement, congratulations. You've amassed enough money to create your own portfolio-generated paycheck. Excellent work. But you can't take it too easy, because you'll receive a severe pay cut if you deplete your portfolio too fast. How much can you take out each year and be almost certain that you won't outlive your savings? Just 4% a year. That's the withdrawal rate that would have sustained a mix of stocks and bonds over most 30-year historical periods. Sure, if you retire on the eve of the next bull market, you can take out more. However, if you quit working right before the next bear market, then taking out more than 4% a year could have your portfolio beating you to the grave.

3. Trying too hard to beat the market. You basically have two choices: You can be a master stock-picker like Warren Buffett or Peter Lynch and try to find the next Wal-Mart. Or you can broadly diversify your assets, mostly via low-cost index funds. This way, you enjoy hefty exposure to all the great companies.

4. Paying too much for help. There's nothing wrong with getting financial advice. But I firmly, strongly, passionately believe that such help should be objective and affordable. Paying too much for advice (especially if it's bad or at least conflicted) does a lot for your broker's retirement, not yours. Paying just 1% a year on a $100,000 portfolio over 20 years could result in your forking over more than that amount in fees. That's a hundred grand that could have been in your pocket. Of course, if the advice you received had your portfolio performing better than what you could do on your own, then the price might be worth it. But if you're paying 1% or 2% a year to lose to an index fund -- as most mutual fund managers do -- then you're better off taking control of your own investments.

5. Retiring permanently when you really just needed a break. If you're in your 60s, you should plan on living at least another two decades. Can you stand full-time leisure for 20 years? Sure, it may sound good now, but many retirees find they get pretty bored after a while. But by then, they have already severed many of their professional ties. Before you decide to retire fully and permanently, discuss a phased or gradual retirement with your employer and/or business partners. Or the possibility of working on a project basis, allowing you to take several months off each year. Or maybe just a one-year sabbatical. Explore your options before you no longer have them.

July 26, 2010

Ten Stock Market Myths That Just Won't Die

Here is a great article I just saw online from the Wall Street Journal, I couldn't say it better myself.

At times like this, your broker or financial adviser may offer words of wisdom or advice. There are standard calming phrases you will hear over and over again. But how true are they? Here are 10 that need extra scrutiny.

1 "This is a good time to invest in the stock market."

Really? Ask your broker when he warned clients that it was a bad time to invest. October 2007? February 2000? A broken watch tells the right time twice a day, but that's no reason to wear one. Or as someone once said, asking a broker if this is a good time to invest in the stock market is like asking a barber if you need a haircut. "Certainly, sir — step this way!"

2 "Stocks on average make you about 10% a year."

Stop right there. This is based on some past history — stretching back to the 1800s — and it's full of holes.

About three of those percentage points were only from inflation. The other 7% may not be reliable either. The data from the 19th century are suspect; the global picture from the 20th century is complex. Experts suggest 5% may be more typical. And stocks only produce average returns if you buy them at average valuations. If you buy them when they're expensive, you do a lot worse.

3 "Our economists are forecasting..."

Hold it. Ask your broker if the firm's economist predicted the most recent recession — and if so, when. The record for economic forecasts is not impressive. Even into 2008 many economists were still denying that a recession was on the way. The usual shtick is to predict "a slowdown, but not a recession." That way they have an escape clause, no matter what happens. Warren Buffett once said forecasters made fortune tellers look good.

4 "Investing in the stock market lets you participate in the growth of the economy."

Tell that to the Japanese. Since 1989 their economy has grown by more than a quarter, but the stock market is down more than three quarters. Or tell that to anyone who invested in Wall Street a decade ago. And such instances aren't as rare as you've been told. In 1969, the U.S. gross domestic product was about $1 trillion, and the Dow Jones Industrial Average was at about 1000. Thirteen years later, the U.S. economy had grown to $3.3 trillion. The Dow? About 1000.

5 "If you want to earn higher returns, you have to take more risk."

This must come as a surprise to Mr. Buffett, who prefers investing in boring companies and boring industries. Over the last quarter century, the FactSet Research utilities index has even outperformed the exciting, "risky" Nasdaq Composite index. The only way to earn higher returns is to buy stocks cheap in relation to their future cash flows. As for "risk," your broker probably thinks that's "volatility," which typically just means price ups and downs. But you and your Aunt Sally know that risk is really the possibility of losing principal.

6 "The market's really cheap right now. The P/E is only about 13."

The widely quoted price/earnings (PE) ratio, which compares share prices to annual after-tax earnings, can be misleading. That's because earnings are so volatile — they're elevated in a boom, and depressed in a bust.

Ask your broker about other valuation metrics, like the dividend yield, which looks at the dividends you get for each dollar of investment; or the cyclically adjusted PE ratio, which compares share prices to earnings over the past 10 years; or "Tobin's q," which compares share prices to the actual replacement cost of company assets. No metric is perfect, but these three have good track records. Right now all three say the stock market's pretty expensive, not cheap.

7 "You can't time the market."

This hoary old chestnut keeps the clients fully invested. Certainly it's a fool's errand to try to catch the market's twists and turns. But that doesn't mean you have to suspend judgment about overall valuations.

If you invest in shares when they're cheap compared to cash flows and assets — typically this happens when everyone else is gloomy — you will usually do very well. If you invest when shares are very expensive — such as when everyone else is absurdly bullish — you will probably do badly.

8 "We recommend a diversified portfolio of mutual funds."

If your broker means you should diversify across things like cash, bonds, stocks, alternative strategies, commodities and precious metals, then that's good advice. But too many brokers mean mutual funds with different names and "styles" like large-cap value, small-cap growth, midcap blend, international small-cap value, and so on. These are marketing gimmicks. There is, for example, no such thing as "midcap blend." These funds are typically 100% invested all the time, and all in stocks. In this global economy even "international" offers less diversification than it did, because everything's getting tied together.

9 "This is a stock picker's market."

What? Every market seems to be defined as a "stock picker's market," yet for most people the lion's share of investment returns — for good or ill — has typically come from the asset classes (see No. 8, above) they've chosen rather than the individual investments. And even if this does turn out to be a stock picker's market, what makes you think your broker is the stock picker in question?

10 "Stocks outperform over the long term."

Define the long term? If you can be down for 10 or more years, exactly how much help is that? As John Maynard Keynes, the economist, once said: "In the long run we are all dead."

And I would add given the above ten myths, that a person shouldn't even really consider investing period unless they have paid off their house!

At times like this, your broker or financial adviser may offer words of wisdom or advice. There are standard calming phrases you will hear over and over again. But how true are they? Here are 10 that need extra scrutiny.

1 "This is a good time to invest in the stock market."

Really? Ask your broker when he warned clients that it was a bad time to invest. October 2007? February 2000? A broken watch tells the right time twice a day, but that's no reason to wear one. Or as someone once said, asking a broker if this is a good time to invest in the stock market is like asking a barber if you need a haircut. "Certainly, sir — step this way!"

2 "Stocks on average make you about 10% a year."

Stop right there. This is based on some past history — stretching back to the 1800s — and it's full of holes.

About three of those percentage points were only from inflation. The other 7% may not be reliable either. The data from the 19th century are suspect; the global picture from the 20th century is complex. Experts suggest 5% may be more typical. And stocks only produce average returns if you buy them at average valuations. If you buy them when they're expensive, you do a lot worse.

3 "Our economists are forecasting..."

Hold it. Ask your broker if the firm's economist predicted the most recent recession — and if so, when. The record for economic forecasts is not impressive. Even into 2008 many economists were still denying that a recession was on the way. The usual shtick is to predict "a slowdown, but not a recession." That way they have an escape clause, no matter what happens. Warren Buffett once said forecasters made fortune tellers look good.

4 "Investing in the stock market lets you participate in the growth of the economy."

Tell that to the Japanese. Since 1989 their economy has grown by more than a quarter, but the stock market is down more than three quarters. Or tell that to anyone who invested in Wall Street a decade ago. And such instances aren't as rare as you've been told. In 1969, the U.S. gross domestic product was about $1 trillion, and the Dow Jones Industrial Average was at about 1000. Thirteen years later, the U.S. economy had grown to $3.3 trillion. The Dow? About 1000.

5 "If you want to earn higher returns, you have to take more risk."

This must come as a surprise to Mr. Buffett, who prefers investing in boring companies and boring industries. Over the last quarter century, the FactSet Research utilities index has even outperformed the exciting, "risky" Nasdaq Composite index. The only way to earn higher returns is to buy stocks cheap in relation to their future cash flows. As for "risk," your broker probably thinks that's "volatility," which typically just means price ups and downs. But you and your Aunt Sally know that risk is really the possibility of losing principal.

6 "The market's really cheap right now. The P/E is only about 13."

The widely quoted price/earnings (PE) ratio, which compares share prices to annual after-tax earnings, can be misleading. That's because earnings are so volatile — they're elevated in a boom, and depressed in a bust.

Ask your broker about other valuation metrics, like the dividend yield, which looks at the dividends you get for each dollar of investment; or the cyclically adjusted PE ratio, which compares share prices to earnings over the past 10 years; or "Tobin's q," which compares share prices to the actual replacement cost of company assets. No metric is perfect, but these three have good track records. Right now all three say the stock market's pretty expensive, not cheap.

7 "You can't time the market."

This hoary old chestnut keeps the clients fully invested. Certainly it's a fool's errand to try to catch the market's twists and turns. But that doesn't mean you have to suspend judgment about overall valuations.

If you invest in shares when they're cheap compared to cash flows and assets — typically this happens when everyone else is gloomy — you will usually do very well. If you invest when shares are very expensive — such as when everyone else is absurdly bullish — you will probably do badly.

8 "We recommend a diversified portfolio of mutual funds."

If your broker means you should diversify across things like cash, bonds, stocks, alternative strategies, commodities and precious metals, then that's good advice. But too many brokers mean mutual funds with different names and "styles" like large-cap value, small-cap growth, midcap blend, international small-cap value, and so on. These are marketing gimmicks. There is, for example, no such thing as "midcap blend." These funds are typically 100% invested all the time, and all in stocks. In this global economy even "international" offers less diversification than it did, because everything's getting tied together.

9 "This is a stock picker's market."

What? Every market seems to be defined as a "stock picker's market," yet for most people the lion's share of investment returns — for good or ill — has typically come from the asset classes (see No. 8, above) they've chosen rather than the individual investments. And even if this does turn out to be a stock picker's market, what makes you think your broker is the stock picker in question?

10 "Stocks outperform over the long term."

Define the long term? If you can be down for 10 or more years, exactly how much help is that? As John Maynard Keynes, the economist, once said: "In the long run we are all dead."

And I would add given the above ten myths, that a person shouldn't even really consider investing period unless they have paid off their house!

July 20, 2010

Analysts Are Not Important to Investors

Analysts are not important to you as an investor. Don’t get me wrong, analysts are important to the financial markets, just not to you as a longer term investor.

Analysts are not important to you as an investor. Don’t get me wrong, analysts are important to the financial markets, just not to you as a longer term investor.Analysts typically work for brokerage firms and express opinions and write reports on the public companies that they follow. They offer different ratings such as buy, hold and sell.

The analysts you regularly see on TV work for brokerage firms (sell side) or investment firms (buy side). They will often times mention their price target for a particular stock and sometimes more vaguely will issue a statement on how a particular stock will perform compared to the market as a whole which is quite weak to say the least. Talk about riding the fence.

Up until recently, analysts did not disclose that they held those stocks in their personal portfolio nor did they have to mention if the firm they work for had received some investment banking fees from that same company they are supposedly impartially reporting on!

You will no doubt have seen an analyst upgrade or downgrade a particular stock due to some important event. What is not widely recognized is that the analyst’s record does not reflect that day’s price action and therefore their record is entirely bogus and unreliable.

Studies show that during the height of the technology bubble in 1999-2000 that over 90% of brokerage firm analysts had buy or strong buy ratings on the stocks they covered at the peak or top of the market.

As a stockbroker, I often times wondered if analyst buy ratings were so the firm could sell inventory to clients? I and you will never know.

Just remember this. There isn’t really any correlation between what happens on Wall Street this morning and your long term investments so ignore the analysts and all the other noise and remain focused on the long term.

July 2, 2010

The Market Is Like a Yo Yo (and thats good)

Ok, its now July and the first half of the year is in the books and the stock market is down over 7%. Thats not so great. Its worse if you paid some financial 'professional' some percentage or fee for those same results.

The stock market is like a yo yo and very long term, its like a yo yo you are holding while going up stairs. No one likes the downturns but they are necessary for you to make money (as long as you have been dollar cost averaging).

Just keep picturing yourself closer to retirement closer to the top of the stairs having reaped the benefits of long term investing, not being sucked in to short term trading scams or get rich quick schemes.

Stay focused and you will get there.

The stock market is like a yo yo and very long term, its like a yo yo you are holding while going up stairs. No one likes the downturns but they are necessary for you to make money (as long as you have been dollar cost averaging).

Just keep picturing yourself closer to retirement closer to the top of the stairs having reaped the benefits of long term investing, not being sucked in to short term trading scams or get rich quick schemes.

Stay focused and you will get there.

June 30, 2010

To Plan Or Not To Plan, That Is The Question

You have seen the commercials on TV, what is your number? You read and hear about financial planning all the time. Here is the skinny.

Of course, you need to plan if that means being somewhat fiscally responsible enough to put money away for your retirement and your kids college.

It does not mean however that you need to sit down with some guy with very little if any experience and plan your life down to the last penny so you come up with an arbitrary number, good grief!

There are just too many variables for you to even remotely plan that well. It sounds good on paper and of course, the investerati, the brokerage and investments firms love it because they can charge you another fee and keep your assets with them because there is absolutely no way you are smart enough to do it on your own, did I already say good grief?

I provide workshops in this area and am shocked at what people think they need to do, how stressed they are and how many boxes they think they need to check. No. Dare I say that it is easy to plan, so much so that I wouldn't even call it a plan and certainly wouldn't charge anyone for the 'advice'.

Of course, you need to plan if that means being somewhat fiscally responsible enough to put money away for your retirement and your kids college.

It does not mean however that you need to sit down with some guy with very little if any experience and plan your life down to the last penny so you come up with an arbitrary number, good grief!

There are just too many variables for you to even remotely plan that well. It sounds good on paper and of course, the investerati, the brokerage and investments firms love it because they can charge you another fee and keep your assets with them because there is absolutely no way you are smart enough to do it on your own, did I already say good grief?

I provide workshops in this area and am shocked at what people think they need to do, how stressed they are and how many boxes they think they need to check. No. Dare I say that it is easy to plan, so much so that I wouldn't even call it a plan and certainly wouldn't charge anyone for the 'advice'.

June 11, 2010

Don't Assume That Time In The Markets Lowers Risk (because it doesn't)

Many investors think that you make the risk of stocks magically go away just by owning them long enough which is simply not true. You hear it all the time, own stocks and think long term.

While everyone knows that since 1926, that stocks have returned approximately 10%, or 8% CAGR, that fact does not help someone who had their retirement invested 100% in stocks over the last few years. Assuming they didn't get scared out near the lows of last year, they are still down 20-30% and possibly as much as 50%.

The moral of the story is do not buy what the investerati are selling, that is, do not subscribe to the idea that you have to own stocks. If you do, be careful. Invest only a portion of those investable assets in stocks. Remember that bonds and CD's are just fine, not very sexy, but have to be a part of your portfolio, a big part of your portfolio, especially as you get closer to retirement.

While everyone knows that since 1926, that stocks have returned approximately 10%, or 8% CAGR, that fact does not help someone who had their retirement invested 100% in stocks over the last few years. Assuming they didn't get scared out near the lows of last year, they are still down 20-30% and possibly as much as 50%.

The moral of the story is do not buy what the investerati are selling, that is, do not subscribe to the idea that you have to own stocks. If you do, be careful. Invest only a portion of those investable assets in stocks. Remember that bonds and CD's are just fine, not very sexy, but have to be a part of your portfolio, a big part of your portfolio, especially as you get closer to retirement.

May 25, 2010

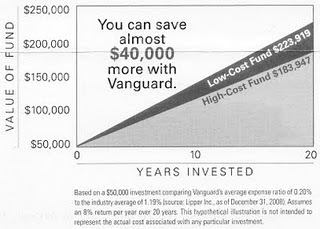

Lower Fees = Money In Your Pocket

I have always said that fees are everything. Here is a marketing piece from Vanguard. I am not a shill, nor do I work with Vanguard but I do like their mutual funds and exchange traded funds (etf's) largely because they are the lowest cost, period.

I

I

own

VTI

myself.

It may be hard to read but this is the comparison of $50,000 invested over twenty years in two funds, both with returns of 8%. The higher cost fund has fees of 1.19% (which is very normal) and is compared with 0.20% for the lower cost fund. You can see that the difference is almost $40,000! This is money in your pocket or not, your choice!

Now I know you like your stockbroker / financial advisor but you are paying him and his firm a ridiculous amount of money for the exact same product. If you like him that much, great, buy him a car because thats about what you are paying.

own

VTI

myself.

It may be hard to read but this is the comparison of $50,000 invested over twenty years in two funds, both with returns of 8%. The higher cost fund has fees of 1.19% (which is very normal) and is compared with 0.20% for the lower cost fund. You can see that the difference is almost $40,000! This is money in your pocket or not, your choice!

Now I know you like your stockbroker / financial advisor but you are paying him and his firm a ridiculous amount of money for the exact same product. If you like him that much, great, buy him a car because thats about what you are paying.

May 20, 2010

Go Away In May They Say, Good Strategy?

Go away in May they say, keep your cash for another day. Thats a great old Wall Street saying which means sell in May and buy again in the fall.

Studies have shown that strategy to be mostly false.

There is a negligible difference as compared to buying and holding and besides, you will incur commissions, costs and fees to sell and buy again in the fall.

Additionally, just like trading, sure its nice when you are right but hurts when you are wrong and unless you have a crystal ball, you end up like the dog chasing his tail and get nowhere.

A great example would have been 2009, it sure looked like after a nice runup from the lows in March after the bear market of 2008-9 that selling in May might be a great idea, well, it wasn't and alot of people sold and missed a massive run since and some never got back in.

While its tempting to try and beat the market (aka S&P 500) just dont. Remember that over 90% of professional money managers can't so your chances are pretty slim.

Studies have shown that strategy to be mostly false.

There is a negligible difference as compared to buying and holding and besides, you will incur commissions, costs and fees to sell and buy again in the fall.

Additionally, just like trading, sure its nice when you are right but hurts when you are wrong and unless you have a crystal ball, you end up like the dog chasing his tail and get nowhere.

A great example would have been 2009, it sure looked like after a nice runup from the lows in March after the bear market of 2008-9 that selling in May might be a great idea, well, it wasn't and alot of people sold and missed a massive run since and some never got back in.

While its tempting to try and beat the market (aka S&P 500) just dont. Remember that over 90% of professional money managers can't so your chances are pretty slim.

May 19, 2010

Do I Really Need A Stockbroker Or Financial Planner?

I am frequently asked the question, do I need a stockbroker, financial advisor or financial planner?

You'd be surprised at the 'training' stockbrokers are given before they start to handle your money, its really shockingly little. Most of the 'training' is on the job which is not ok with my money, maybe you are ok with that. Your decision of course.

Given the wealth of resources available online and the fact that even the discounters such as Fidelity, Schwab, TD Ameritrade and Scottrade have advisors that you can lean on for advice for free, it really doesn't make sense to pay anyone for something you can do for yourself. You pump your own gas right? You buy your own groceries!

People will say that it takes too much time which is simply not true. I think some people just don't want to make decisions for themselves and want to have someone to blame if things go wrong. That's fine as long as you don't mind paying 5-10 times for the same exact service and that you go into the relationship knowing what you are paying for. If you feel thats a value for you great then go ahead.

Make no mistake, the broker-client relationship is like other relationships, in that its hard to breakup which might make you stay after you realize there is little value which ends up costing you more and more.

Also, fees are the most important factor in investment success, not which investments you pick (something the investerati would have you believe they can do and you can't) and not timing (which some people believe they can do but have never proven it).

And stockbrokers and financial planners will be the first to tell you that they are not tax or legal experts and that you will need consult those experts as well as them so given that, what exactly does your financial guy do for you anyway?

So the answer to the question is that it depends on you but my opinion is that you do not need the advice of a stockbroker or financial planner. You can acheive the same or better results by yourself.

You'd be surprised at the 'training' stockbrokers are given before they start to handle your money, its really shockingly little. Most of the 'training' is on the job which is not ok with my money, maybe you are ok with that. Your decision of course.

Given the wealth of resources available online and the fact that even the discounters such as Fidelity, Schwab, TD Ameritrade and Scottrade have advisors that you can lean on for advice for free, it really doesn't make sense to pay anyone for something you can do for yourself. You pump your own gas right? You buy your own groceries!

People will say that it takes too much time which is simply not true. I think some people just don't want to make decisions for themselves and want to have someone to blame if things go wrong. That's fine as long as you don't mind paying 5-10 times for the same exact service and that you go into the relationship knowing what you are paying for. If you feel thats a value for you great then go ahead.

Make no mistake, the broker-client relationship is like other relationships, in that its hard to breakup which might make you stay after you realize there is little value which ends up costing you more and more.

Also, fees are the most important factor in investment success, not which investments you pick (something the investerati would have you believe they can do and you can't) and not timing (which some people believe they can do but have never proven it).

And stockbrokers and financial planners will be the first to tell you that they are not tax or legal experts and that you will need consult those experts as well as them so given that, what exactly does your financial guy do for you anyway?

So the answer to the question is that it depends on you but my opinion is that you do not need the advice of a stockbroker or financial planner. You can acheive the same or better results by yourself.

May 4, 2010

Personal Finances and Productivity

There is an inverse relationship between time spent on personal finances and both productivity and investment returns. Have your cake and eat it too!

Most everyone has heard that people spent a lot of time at work goofing around. The number one time killer to no ones surprise is technology. Time wasted surfing the Internet, etc. But the number two time killer in the workplace is a surprise to most and that is the time employees spend on their personal finances. This can be time chatting with a friend about a hot stock, trading stocks online, filling out a mortgage application, debt consolidation, etc. I have even seen studies showing some people rebalance their 401k everyday!

Studies show that people spend as much as 30-45 minutes a day on their personal finances, thats as much as half a work day each week! Everyone understands that you have to have a life and that sometimes, personal stuff has to be done during normal work hours however few employers are ok with you trading stocks during the day.

The irony is that the more time spent trading, rebalancing your retirement accounts and talking to a stockbroker are all detrimental to your fiscal health. Every study on the subject conclusively proves that passive investing beats active investing. In the book, How The Investment Business Really Works and in my workshops, I go into much greater detail as to exactly what people should be doing and more importantly, what they shouldn't be doing.

Moral of the story is to place your investable assets in the lowest fee possible index fund and leave it alone. With that simple strategy, you will beat over 90% of the 'professional' money managers AND you will be more productive at work in addition to having less stress!

Most everyone has heard that people spent a lot of time at work goofing around. The number one time killer to no ones surprise is technology. Time wasted surfing the Internet, etc. But the number two time killer in the workplace is a surprise to most and that is the time employees spend on their personal finances. This can be time chatting with a friend about a hot stock, trading stocks online, filling out a mortgage application, debt consolidation, etc. I have even seen studies showing some people rebalance their 401k everyday!

Studies show that people spend as much as 30-45 minutes a day on their personal finances, thats as much as half a work day each week! Everyone understands that you have to have a life and that sometimes, personal stuff has to be done during normal work hours however few employers are ok with you trading stocks during the day.

The irony is that the more time spent trading, rebalancing your retirement accounts and talking to a stockbroker are all detrimental to your fiscal health. Every study on the subject conclusively proves that passive investing beats active investing. In the book, How The Investment Business Really Works and in my workshops, I go into much greater detail as to exactly what people should be doing and more importantly, what they shouldn't be doing.

Moral of the story is to place your investable assets in the lowest fee possible index fund and leave it alone. With that simple strategy, you will beat over 90% of the 'professional' money managers AND you will be more productive at work in addition to having less stress!

April 26, 2010

Still Paying Mutual Fund Commissions???

I come across a myriad of investors in my workshops and the question of mutual fund commissions still arises and continues to amaze me. Don't take this the wrong way because I understand this is a business I understand well and most don't but please use common sense! Heck I'm no mechanic but when I go to get my oil changed and the guy says, that'll be $475, I know something isn't right.

As recently as the early 90's, stockbrokers got paid as much as 8.5% of the total investment to steer clients towards a particular mutual fund! Insurance guys still see those kinds of commissions.

Believe it or not, stockbrokers and financial advisors still get paid as much as 5% for some mutual funds and sometimes this fee is taken out of the original principle which means all of your money isn't going to work immediately, this ought to be a crime. When the 5% is not seen or 'hidden', clients are told not to worry, there is no commission, arrgghhh!

What happens is that the mutual fund wants the money back that they paid to the stockbroker or financial advisor. Either one of two things; that mutual fund will be charging you 1-2% a year more or there is a lock up period whereby if you sell that mutual fund, you will be assessed a fee. Neither is good and both are bad.

What to do? If you are convinced you need to own a mutual fund, ok, then, look for;

As recently as the early 90's, stockbrokers got paid as much as 8.5% of the total investment to steer clients towards a particular mutual fund! Insurance guys still see those kinds of commissions.

Believe it or not, stockbrokers and financial advisors still get paid as much as 5% for some mutual funds and sometimes this fee is taken out of the original principle which means all of your money isn't going to work immediately, this ought to be a crime. When the 5% is not seen or 'hidden', clients are told not to worry, there is no commission, arrgghhh!

What happens is that the mutual fund wants the money back that they paid to the stockbroker or financial advisor. Either one of two things; that mutual fund will be charging you 1-2% a year more or there is a lock up period whereby if you sell that mutual fund, you will be assessed a fee. Neither is good and both are bad.

What to do? If you are convinced you need to own a mutual fund, ok, then, look for;

- no load mutual funds

- no lock up period whereby selling incurs a cost

- very low fees lower than 0.5%

April 21, 2010

Dollar Cost Averaging Is Why 401k's Work and Buying Individual Stocks Doesn't

Dollar cost averaging (and time) is exactly why 401k's are so successful. People mindlessly (in a good way) add to a diversified portfolio when its up, and when its down.

Buying more when your individual stock goes down is exactly why people rarely make money outside of 401k's. You know the scenario, you buy XYZ and it goes down, you buy more and more and again and again until your portfolio has ten or fifteen losers in it. You hold until breakeven (if you are lucky) and sell, whew, only to try again, most times with the 'aid' of a stockbroker.

Thats why I tell people to buy no load mutual funds or etf's and treat monies inside and outside of 401k's the same. Its a winning strategy so don't mess with it.

Buying more when your individual stock goes down is exactly why people rarely make money outside of 401k's. You know the scenario, you buy XYZ and it goes down, you buy more and more and again and again until your portfolio has ten or fifteen losers in it. You hold until breakeven (if you are lucky) and sell, whew, only to try again, most times with the 'aid' of a stockbroker.

Thats why I tell people to buy no load mutual funds or etf's and treat monies inside and outside of 401k's the same. Its a winning strategy so don't mess with it.

April 6, 2010

Emerging Markets and Overseas Investing

I am asked on occasion about investing in emerging markets. While it is tempting to invest in markets such as China, India, Brazil, Korea, Russia, etc, it is also quite risky.

Risks inherent to investing in companies in countries outside the US include;

In my opinion, the reward does not outweigh the risk and besides that, the fees within mutual funds or etf's that deal in emerging markets and overseas markets are quite high and if you have been following this blog for any amount of time, then you already know what I think of fees. Arrghh.

Stick to a domestic index fund, keep your fees super low and emotions in check and you are doing about all you can. With that simple strategy, you will beat 90% of the people including investment professionals.

Risks inherent to investing in companies in countries outside the US include;

- less stringent reporting requirements

- currency fluctuations

- government regulation and policy changes

In my opinion, the reward does not outweigh the risk and besides that, the fees within mutual funds or etf's that deal in emerging markets and overseas markets are quite high and if you have been following this blog for any amount of time, then you already know what I think of fees. Arrghh.

Stick to a domestic index fund, keep your fees super low and emotions in check and you are doing about all you can. With that simple strategy, you will beat 90% of the people including investment professionals.

April 1, 2010

Mirror The Index's And Save Money

Fact - over 90% of financial professional money managers cannot beat the S&P 500 nor the Dow Jones 30.

Fact - with a stockbroker, advisor or planner, you will pay a lot in fees, sometimes 1%-3% just to get the same or lower returns.

See the chart to the right, VTI (blue) and Dow Jones 30 (red). VTI is vanguards total market return etf which I own personally but any market based etf or mutual fund will do. They all mirror the indices as you can see which will outperform over 90% of the so-called financial professionals who will charge fees for that underperformance!

The fees on this particular etf are .07%, thats right, less than 1/10th of 1%.

Stop being the 'stupid money' stockbrokers refer to when you open up your account with them and start being the smart money who beats 90% of all investors and pays less to do it.

March 24, 2010

Approach To Investing

Your approach to investing has to change if you think you can time the market. I just read an article at yahoo finance which backs up what I've known for years, that timing the market is virtually impossible.

Research for the twenty year period 1983-2003 is below. Pay attention and learn something that you may not already know and certainly your stockbroker or financial advisor is not telling you.

1983-2003 period for S&P 500

Buy and Hold = 10%

Minus the 30 worst days = 19%

Minus the 20 best days = 5%

Moral of the story is that if you are willing to risk missing the best days trying to miss the worst days, go ahead but you will have probably wasted a lot of your time, and money and got nowhere. You need to change your approach to investing.

I have said it before and will say it again, buy a no-load mutual fund or ETF that tracks the S&P 500 and you are doing really all you can do.

March 23, 2010

If Its Too Good To Be True .........

People will ask me about investing in pink sheet stocks (.pk) or over the counter bulletin board stocks (.bb) from time to time and my answer is always the same, I have yet to see anyone make any money buying them. So run, dont walk away from anyone who is offering to sell you anything like that.

I have been around stocks for almost three decades and the story is always the same, its a small company with a great product that just needs funding. Maybe something to do with China or India. Biotech and a cancer cure always generates some buzz. Homeland security is new. JUNK. I know the stories sound good but so does Dr. Seuss.

If the company actually had a real product, they would go the private equity route to fund their needs but those guys are far too smart for that junk. So the peddlers of pink sheet and otcbb companies have only the regular investing public to prey on. Stay away.

I have been around stocks for almost three decades and the story is always the same, its a small company with a great product that just needs funding. Maybe something to do with China or India. Biotech and a cancer cure always generates some buzz. Homeland security is new. JUNK. I know the stories sound good but so does Dr. Seuss.

If the company actually had a real product, they would go the private equity route to fund their needs but those guys are far too smart for that junk. So the peddlers of pink sheet and otcbb companies have only the regular investing public to prey on. Stay away.

March 12, 2010

Saving For Retirement

When you retire, you will be living on your savings and income from social security (hopefully). Thats about it. Hopefully you will have a lump sum from years of savings and its common thought that you can spend about 4-5% of your nestegg every year (without any growth, thats 20-25 years after retirement day).

I know there are a gazillion financial calculators on the Internet (I like yahoo finance as a source) but quite frankly, there are just too many variables to bother and do not let a financial advisor charge you for this. Will my kids need money? What will healthcare cost? What will taxes be? What kind of return can I expect? Divorce? Lawsuit? Inheritance?

Now, you can't and shouldn't count on any growth (ask a recent retiree) but very long term, the S&P 500 has returned just over 8% so if you have a portion in the S&P 500 and most in safe govt bonds or CD's, you will probably end up near 3-4%.

You may not touch the principle some years and of course, some years, you will. Again, its nice to plan but the large amount of variables outweigh any real planning you can do so don't stress too much.

Bottom line. Save the most you possibly can and keep fees very low (I like Vanguards S&P 500 exchange traded fund symbol VTI) and as you approach retirement, you will have a much better idea as to how much that 4-5% a year will be. It will then be time to plan and adjust your lifestyle to match what you have.

March 10, 2010

Same Old Story

Turn on the TV, read the paper or talk to any financial advisor and you will hear the same people repeating the same old story over and over and over again. YAWN.

Not one of these guys can beat the S&P 500!!! Their goal is to appear more intelligent than you, get some exposure on TV for their firm so that you will continue to give them your money for which they receive some nice fees, only to underperform the market time and time again.

- The market will be volatile until its not

- This is a stock pickers market

- You need to own this sector and not that one

- We are buying the big diversified multi-nationals

- The market is overpriced / underpriced

Not one of these guys can beat the S&P 500!!! Their goal is to appear more intelligent than you, get some exposure on TV for their firm so that you will continue to give them your money for which they receive some nice fees, only to underperform the market time and time again.

March 2, 2010

Are Mutual Fund Returns Really What They Say???

Ok, you hear about this great mutual fund and you jump in. First year it returns 100%, nice, very nice. The second year isn't so good, down 50%. The mutual fund then claims an average return of 25% which is technically true if you just do the math and average the two years.

However, if you were a shareholder for both of those years, your return is 0%. Whatever you gained in the first year was wiped out in the second. Its called CAGR which is compound annual growth rate which is the 'real' or annualized return.

As an investor, you need to be wary of many things, only one of which is the 'return' a mutual fund or your stockbroker claims to have acheived.

Since 1990, the stock market (as judged by the S&P 500) returned 10.16% but a CAGR of 8.23%. That is a massive difference and is rarely discussed.

However, if you were a shareholder for both of those years, your return is 0%. Whatever you gained in the first year was wiped out in the second. Its called CAGR which is compound annual growth rate which is the 'real' or annualized return.

As an investor, you need to be wary of many things, only one of which is the 'return' a mutual fund or your stockbroker claims to have acheived.

Since 1990, the stock market (as judged by the S&P 500) returned 10.16% but a CAGR of 8.23%. That is a massive difference and is rarely discussed.

February 24, 2010

Productivity and Your Finances

Too many people spend too much time on their personal finances, whether its rebalancing their 401k, talking to guy down the hall about a hot stock or worst of all, trading stocks.

This is wasted productivity, not only for the employer but for the employee since every study on the subject conclusively proves that the more time messing around with your finances lowers your returns.

Passive investing beats managed investing all the time.

90%+ of professional money managers cannot beat the S&P 500 so quit paying them fees for nothing.

Moral of the story, leave your 401k alone, dont trade stocks, dont try to beat the market. Get back to work because that 15-20 minutes everyday adds up, in fact, it works out to be a difference in productivity of plus (or minus) of 6%.

If your an employer and your employee asks for a 6% raise because they want to trade stocks on your time, would you say, yeah sure, no problem, of course not. But thats what you are doing by not addressing this problem.

This is wasted productivity, not only for the employer but for the employee since every study on the subject conclusively proves that the more time messing around with your finances lowers your returns.

Passive investing beats managed investing all the time.

90%+ of professional money managers cannot beat the S&P 500 so quit paying them fees for nothing.

Moral of the story, leave your 401k alone, dont trade stocks, dont try to beat the market. Get back to work because that 15-20 minutes everyday adds up, in fact, it works out to be a difference in productivity of plus (or minus) of 6%.

If your an employer and your employee asks for a 6% raise because they want to trade stocks on your time, would you say, yeah sure, no problem, of course not. But thats what you are doing by not addressing this problem.

February 18, 2010

1%

See the chart off to the right from the SEC.gov. This shows what the difference is between paying 1.5% and 0.5%. After 30 years (and we should all be long term investors) at average return of 8% with an initial investment of only $10,000. The difference is $22,634 in your pocket!

Many investors utilize a stockbroker or financial advisor for advice and of course, thats not free, usually the fees range from 1-3%. So now consider that for every $10,000 you hand over to a stockbroker or financial advisor, after 30 years, you will have given them well over $20,000.

Its a lot of money, a huge cost which lowers your investment returns in a big way so you better be sure you are getting something in return, some great advice, some hand-holding during the tough times, etc. but just don't expect higher returns.

Fact is that over 90% of professional money managers cannot beat the S&P 500 with any consistency.

So just keep it in the back of your mind that while paying for advice may seem like a good idea, and sometimes it is, just remember that 1-2% is a lot of money over time and only you can decide if the advice you are getting is worth it.

February 17, 2010

Trading is Gambling, Period.

I was a stockbroker and a trader. The best clients, those that generated the most commission, were always trading their account, buying stocks they thought they knew something about only to sell them shortly thereafter. These days with flat fee accounts, there is no commission incentive but trading is still a terrible strategy.

Here's what happens. You buy a stock because you think you know something about a company, their products or services, the mgmt, etc. (all of which doesn't matter unless you plan to hold it for a long period of time, more than two or three years).

The stock then goes up and you sell for a quick profit, great.

Or it goes down and you hold it, waiting for it to return your buy price, sometimes it does and you sell.

Or it goes down a lot and you are stuck.

This is a terrible strategy. At the end of the day, your account is full of losers, not winners.

Trading is gambling, period.

Here's what happens. You buy a stock because you think you know something about a company, their products or services, the mgmt, etc. (all of which doesn't matter unless you plan to hold it for a long period of time, more than two or three years).

The stock then goes up and you sell for a quick profit, great.

Or it goes down and you hold it, waiting for it to return your buy price, sometimes it does and you sell.

Or it goes down a lot and you are stuck.

This is a terrible strategy. At the end of the day, your account is full of losers, not winners.

Trading is gambling, period.

February 5, 2010

Warren Buffett

Unless you've been living under a rock, you know the name Warren Buffett who is one of the rare individuals / institutions that have beaten the S&P 500 with some consistency. If you like him, and its hard not too, you are in luck, you can invest side by side with Warren Buffett by owning his companies shares (Berkshire Hathaway) which is listed at the NYSE as brk-b.

Interestingly, Buffett obviously has a vested interest in his companies shares but for his personal account, he buys US treasuries!

January 11, 2010

Book Seen On TV

How The Investment Business REALLY Works! is a ground breaking book long overdue.

How The Investment Business REALLY Works! is a ground breaking book long overdue. The author came from a very successful career working for wall street's biggest firms and knows how wall street works and how the investment business really does work!

Barclay shares the 'secrets' of the investment industry as few can and fewer do.

Most speakers in this area are still compensated for selling products. Barclay offers investment advice without an agenda, ie. does not sell any investment products and receives no compensation from any advice or discussion presented.

Barclay is happy to give back and loves to educate people on how wall street works, how to invest for yourself, what to do and especially what not to do.

If you'd like a free eChapter, email free@howtheinvestmentbusinessreallyworks.com and check your inbox.